What Current Middle East Military Activity Could Mean for U.S. Business Aviation

Recent U.S. and Israeli military activity in the Middle East introduces another layer of uncertainty into international aviation planning. For U.S. business aviation, the effects are likely to be uneven. Some operators may feel minimal impact. Others, particularly those operating long range international missions, could see meaningful changes in routing, cost, and risk posture.

Below is how this situation could influence the market if tensions persist or expand.

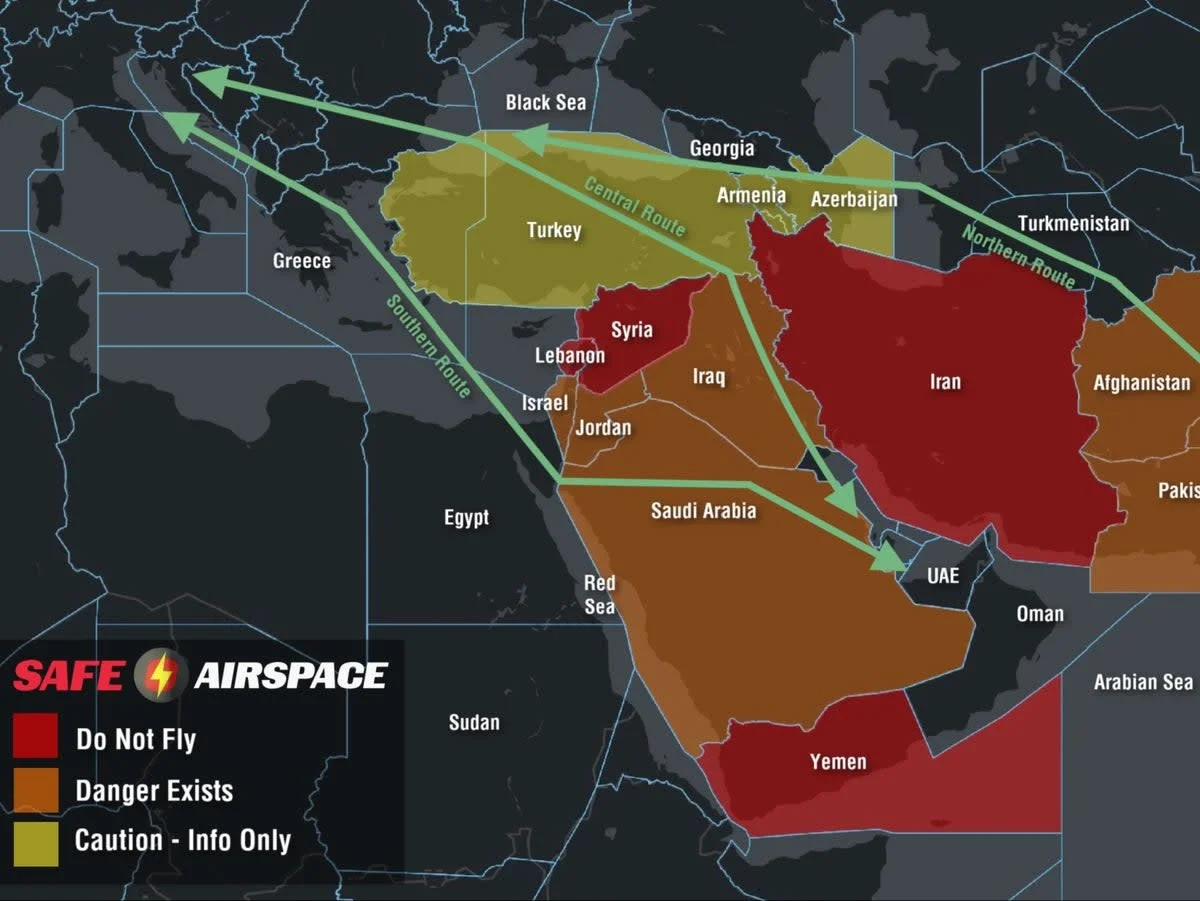

Where the Impact Could Be Direct

The clearest operational exposure sits with missions involving:

U.S. to Middle East

Europe to Middle East

Europe to India and South Asia

U.S. to India routings that would otherwise transit Middle Eastern airspace

If additional airspace restrictions are imposed or existing ones tighten, traffic may be funneled into fewer viable corridors. That could mean longer routings, higher fuel burn, and in some cases added tech stops. It may also compress dispatch timelines as NOTAMs evolve quickly.

None of this would be unprecedented. The industry has adapted to similar patterns over the past several years. The question is duration and scale.

What About U.S. to Europe?

As expected, for most nonstop U.S.–Europe missions, the direct impact would likely be limited.

North Atlantic crossings do not transit Middle Eastern airspace. From a routing standpoint, those flights should remain largely insulated unless the conflict expands geographically.

There are, however, a few indirect channels worth watching.

Europe–Asia traffic displacement

If Middle Eastern corridors become constrained, Europe–Asia traffic may reroute north or south. That could increase congestion in certain European or Eastern Mediterranean airspace sectors. The North Atlantic itself would likely remain unaffected, but major European hubs might experience incremental sequencing or slot pressure during peak disruption periods.

Onward legs beyond Europe

For missions structured U.S. to Europe and then onward to the Gulf, India, or parts of Africa, the second leg becomes more sensitive. Fuel planning, alternates, and crew duty calculations could shift. In that scenario, the exposure sits with the Europe–Middle East segment rather than the Atlantic crossing.

For operators focused strictly on transatlantic corporate flying, the operational effect could remain marginal.

Fuel and Insurance Variables

Even if routing remains unchanged, cost assumptions could move.

Energy markets tend to react to geopolitical risk in major oil producing regions. Sustained escalation could place upward pressure on jet fuel pricing. For long range operators, relatively small market shifts can translate into noticeable trip cost differences.

Insurance markets may also reassess exposure depending on how the conflict develops. Operators flying into or near affected FIRs could see additional scrutiny or revised terms. Those operating domestically or strictly across the North Atlantic may see limited direct impact, though broader market sentiment can influence underwriting behavior over time.

Navigation and Communications Considerations

One operational factor that sometimes emerges in regional conflict environments is GPS interference. If activity increases in certain areas, crews operating nearby may need to be prepared for jamming or spoofing scenarios. That would primarily affect flights operating into or near the region, not typical North Atlantic missions.

Middle Term Outlook

If tensions remain contained and localized, the industry would likely continue adapting through revised routing, conservative fuel planning, and more active risk monitoring.

If the conflict expands materially or persists over a longer horizon, planning assumptions could shift more permanently. Reroutes may become standard practice. Additional fuel margins may be treated as baseline rather than contingency.

At this stage, much depends on duration, geographic spread, and regulatory response.

Bottom Line

For U.S. business aviation, current Middle East military activity could increase complexity and cost for operators tied directly to the region. Pure U.S.–Europe flying would likely remain largely insulated from a routing perspective, though indirect cost and congestion effects are possible.

The situation is fluid. The practical implications will hinge less on headlines and more on whether restrictions expand, fuel markets remain volatile, and insurers adjust their posture.

For now, this looks more like a scenario requiring disciplined planning rather than a structural shift in the market.